The ability to manage personal finances is of utmost importance for individual and family wellbeing. People are most likely to avoid financial problems if they keep track of their financial transactions, have a plan and make informed decisions. Financial literacy is an essential step toward financial freedom which requires the development of good financial habits through practice and self-discipline.

Data from our 2018 personal financial management survey in the Gambia shows a gap in financial literacy among youths.

The survey was conducted in 2018 via an online poll among 139 Gambians between ages 18 and above, of which 95 per cent have acquired at least a college diploma qualification.

Savings Culture and Financial Satisfaction

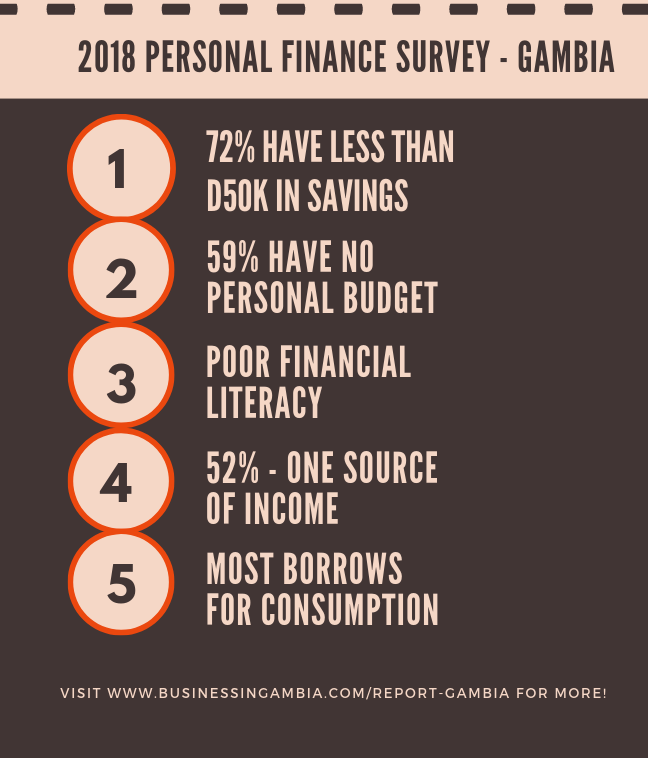

The report highlights that around three in five participants do not prepare a budget, while only three in ten have more than D50,000 ($1,000) in their savings and short-term investment account. More than half of the respondents are not satisfied with their current financial condition. On a scale of 5, the average satisfaction rate was 2.45. Furthermore, out of the respondents who are not happy with their financial conditions, six out every ten are youths. The report also shows that women save more than men.

Personal Financial Budget

The data shows that 59 per cent of respondents does not prepare a personal or family budget. Considering the concept of the personal budget as a tool for managing expenses, it shows that most of the respondents do not plan on how to spend or allocate their money.

6-in-10 postgraduate respondents prepare personal budget compared to 2-in-10 HND holders. This analysis shows a positive relationship between education and appreciating the need for a personal budget. One major reason that influence individuals desire to prepare a budget has to do with their financial education. When people appreciate the importance of a budget, then the preparation and monitoring will be less bored.

Financial Literacy

Through a survey of the most populous countries in the world, India, and Indonesia, Cole et al. (2010) present evidence that financial literacy is an important predictor of financial behaviour in emerging market countries. In a study conducted by Behrman et al. (2012), it was concluded that financial literacy is positively and significantly associated with total net wealth.

Even with 70% graduated respondents, the report reveals that many of the respondents are not financially literate as only 6-in-10 were able to answer both questions about inflation and compound interest correctly. Gender gap issue was also found in financial literacy as male respondents were more financially literate than the females.

Similarly, our study also found that financial literacy is positively related to formal education. High school and college graduates had an average score of 28.57% and 66.18% respectively in financial literacy test compared to the 71.57% and 84.04% average score for the bachelor and postgraduate degree holders respectively in the same test. Similarly, the average score among the youths was 65.73% while the adult respondents had 83.67% average score.

Income sources

The result shows that 52.52% of the respondents have only one stream of income. Additionally, the survey shows a positive relationship between personal financial satisfaction and the number of income streams. Employment is the primary source of income for most educated people in the Gambia. However, the survey shows a positive relationship between the number of income streams and balance in the respondents’ savings account. The respondents who have multiple income streams have higher savings account balances than those with only one source, particularly employment only. 54.79% of the respondents with one source of income are dissatisfied with their financial condition while only 14.29% of the respondents with more than three income sources feel dissatisfied.

Borrowings Habits

Financial well-being can be achieved through extra income, savings and managing expenses. However, these efforts can be wasted if individuals pile debts upon debts. Only 24% of the survey respondents said they have borrowed for investment while 40.67% borrowed for consumption. Most employees have borrowed money for consumption when compared to the self-employed. 47.71% of employees said they have borrowed for consumption and only 26.61% borrowed to invest. On the other hand, among the self-employed, 18.18% borrowed to consumed, 22.73% for invest and 59.09% did not borrow in the last three years.

Insurance

Wealth protection through insurance is not common among Gambians, and the few who buys insurance are mostly to protect motor vehicles where they have no choice but to comply with the law. Over half of the respondents (51.80%) did not buy an insurance policy in the last 12 months. Furthermore, 39.57% of respondents have bought motor vehicle insurance compared to 12.95% for health insurance and 3.6% for properties.

When the respondent’s education level is compared to the insurance purchased, 70.21% of the respondents with a post-graduate degree says they have bought at least one insurance product compared to 32.35% of the HND/College respondents. The respondent’s education level, awareness, and income level may explain the gap between the two groups.

Conclusion and Recommendation

Financial freedom is important to economic growth as we all strive for a more inclusive society. However, financial freedom can be achieved through the application of the best financial management practices. For people to apply personal financial management practices they will need some form of financial education.

Overall, Gambians demonstrate low levels of financial literacy and have difficulty applying financial decision-making skills to real-life situations. Most people are not planning through savings and personal budget and also relies on only one source of income. For a few people who have access to credit, “borrowing to consume” is the most common reason.

For people to apply personal financial management practices they will need some form of financial education. Therefore, the report recommends, amongst others, the involvement of the Gambia’s regulators, policymakers, academics as well as the private sector in the further study, design and implementation of financial literacy programmes in the Gambia.

About the Survey

The Personal Financial Management Survey was conducted online within the Gambia. For complete report and methodology, please download the free full report at www.businessingambia.com/report-gambia