Do you ever wonder why many people are still living on salary to salary even after working for several years? Well, the common answer is the number of dependents. However, I disagree in most cases, because most of these peoples have no proper financial or wealth creation plan. Again, some people think that wealth creation requires some special magical formula which is beyond their imagination. In fact, in some societies, wealthy people are either accused of dealing with politicians or one kind of devil’s money.

Success in wealth creation requires sound strategies, hard work and timely execution. It is essential to understand that wealth cannot be created by just wishing or hoping. You need to take advantage of the basic wealth creation equation, which is the relationship between one’s spending to incomes. In this article, we will discuss the influence of expenses and savings on wealth creation. Wealth here can simply be explained as your net worth ( total assets less Owings).

Let assume that you have no asset or liabilities (owing someone) and you have just received your first salary of D1,000. Your wealth will jump from zero to D1,000. If you spent D750 and deposit D250 into your savings account, then your new wealth position is D250. This is a good start because you have saved 25% of your salary for any future use. Of course, some people are saving 40%, 5% or even 0% of their income. Therefore, a person of the same salary, who saved 50% will be wealthier than you, but you are also better than someone who saved nothing.

The concept is straightforward – the more you save, the more you create wealth for yourself. It does not matter whether you are an entrepreneur, employee or a consultant, in the long run, it is savings that differentiate the wealthy from the rest — the same principle work for companies and even for countries. If a firm earns revenue and spends the whole amount, then there will be no profit to be reinvested in the growth of the company. In fact, loss-making companies do not last long. So, if an individual received a salary and spend everything, then there will be no fund for investment, which leads to strong financial independence.

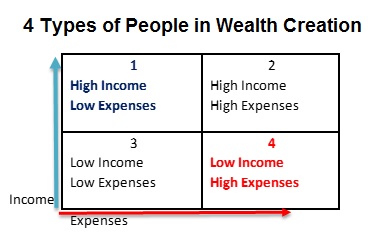

Relationship between Savings and Wealth Creation

In other to show the relationship between savings and wealth creation, we will categorise people into four groups based on their expense to income ratio:

1. High income and low expenses – Financial Planners

The financial planners are people who often save a large chunk of their income for the future. Their wealth keeps on growing year on year due to a higher level of savings. They keep their expenses under control, usually with a personal budget. Their higher accumulated savings are usually turned into a good investment portfolio. Imagine of Omar who earns D40,000 per month and saves D10,000 per month. If he continues saving the same amount for 5 years, his savings account will be D600,000 without considering the compounding of the earned interest. This amount can be used to start a business, develop himself, pay for school fees or for many other reasons why people save money. Many people want to be part of this group but only a few are working towards it.

Tips: If you are in this group, you should continue to save more money and keep on creating wealth but never abandon your basic needs. I am sure you are building the wealth for a purpose. Also, give your time and money to causes that can better our society and the world.

2. High income and high expenses – Enjoyment Group

This is not a bad group but also not the best practice for one to follow. These people earn a higher income, but they also spend almost everything. They usually spend it on expensive lifestyles such as food away from home, frequent travel, rent and entertainments. An increase in the number of peoples in this group is a positive development for most industries. Yes, because the more they spend, the more the business make sales.

People in this group enjoy their money with very little consideration for the future, which means that they are also not good at wealth creation. An example says Doyin, who earns D40,000 per month but she spends at least D39,000 in a month. In 5 years, her savings should be D60,000 again without the interest. This is not encouraging at all. So if Doyin is laid off today or her business collapsed, this D60,000 will be the only asset for her normal lifestyle?

Again their net worth’s are usually very low or sometimes negative. Because they can easily spend more than their income by taking temporal overdrafts in banks. They have the potential to create wealth and most times when you meet them, you will think they are wealthy.

Tips: Control your cost and be yourself. You need to set financial goals and start working on them. A well managed personal budget could improve your financial condition. Remember, this condition and environment may change tomorrow, and your financial independence might be threatened.

Dry your clothes whiles the sun is shining – An African quote

3. Low income and low expenses – Simple life:

Due to their income level, many people in developing countries found themselves in this group. They are the lower income earners but also manage to stay within their means. That is simplicity. They almost spend all their income on necessity such as food, clothing, shelter and health. They have very little or no surplus for wealth creation purpose. With some empowerment and financial education, they have the potential to be in group 1 ( the financial planners).

Tips: Your best option is to look for additional sources of income through self-development, small business or part-time job. Learn about personal finance and set a clear goal on how to increase your income. If you are working, then think about education for better job package or to grow your business. If you cannot increase the family wealth, then work harder and educate your kids.

4. Low income and higher expenses – Keeping up:

The worst are the people who spend the money they have not earned.

These people are usually living their life with competition, fear and emotional issues. They either have periodic overdrafts in their bank accounts or with non-value adding personal loans. For example – taking a loan to buy an old car which will suck their bank accounts through periodic repair bills. If they cannot get bank loans, they usually move to their families and friends to maintain their lifestyle. If you do a background check on them; in most cases, they try to keep up with their co-workers, neighbours, or peers spending patterns.

You should not be earning D5,000 a month, and you want to live in a D8,000 lifestyle. Instead of creating value for the future, you are destroying it now. Staying within one’s income level is a sign of financial discipline.

Tips: Identify your needs from wants and control your desires. Be prepared to change and understand that improving your financial situation could lead to lower emotional stress. Borrowing a loan for consumption means you are spending your future income.

Question – Which wealth creation group do you belong to?

Where are you as at now and where do want to be? Group 1 or 4. No matter where you find yourself in the above quadrants, you have two choices to improve your financial health:

- Increase your sources of income and

- Control your expenses, which leads to more savings.

At your best, rather than looking for one hundred reasons why you cannot save, you should look for one reason why should start saving from today. You can read our ten reasons why we should all save some money.

Must of all you need support and environment that is conducive for what you intend to do

Almost every environment is conducive to create wealth. For every problem, there is always an opportunity.

Expenses are choices we make. Our live style is a choice. Do not think these are excuses not to save. To succeed is about sacrificing one think for the other. Sometimes its just not possible to have it both ways. Planing or lack of it separates the 2 groups in my view.

I agree with you Yanks but on very few occasions. In life, it is easier to give excuse than to see opportunity. You will be surprise that most of the higher expenses are in fact not gift to others. Note that giving is also a fundamental principle in personal finance .

Thank you Sawaneh EB

You are always welcome Salimatou Fatty

Some very good perspectives on wealth creation. These theories work well with people with disposable income; when (critical) expenses, food, clothing, medical and education expenses are less than net, (after tax) income. Ideally, it is necessary to safe for financial security, but sometimes income level versus expenses make it impossible, no matter how thin one stretched their income.

Thank Jallow Mathew. You are right that the income to basic expense can be very close. These are group 3 people. However, the major issue is the group 2 and 4.

Your presentation was well done , personal wealth creation is not a magic all ONE need is FINANCIAL

DISCIPLINE.

Well said Ebrima. Discipline is the keyword to success in any activity.

Great article here Ebrima! I stumbled upon your link on Facebook and I chose to check out your blog. Keep up the good work bro! Africa and the world in general need more people like you.

Thank you Kayode. I am happy you found the blog very educative.

My opinion is that one should be creative by engaging yourself in different activities like one teacher who engages himself in gardening and the cultivation of rice during the rainy season, he does not buy a bag rice for the whole year instead he depends on the rice he grow there by saving money and he also engaged on the weekly trade fair locally known as lumo and within a period of 5years he was able to buy a plot and build a house avoiding the cost of house rent.

Great idea Muniru. We all need to create alternative sources of income. Salary can sometimes create fear in our minds. A small business or weekend job could go a long way.

Very interesting and educational, I see this to help my future and I am glad to come across this piece… Thank you very much for sharing ur beautiful knowledge

I feel fulfilled when someone found the articles useful, much more expressing their appreciation. Thank you Maiumuna

for me in business if am to buy a product for example D10 dalasi and sale it for example D12 i still consider my profit as D0.50b and my simple reason is the other D0.50b Will use as my fuel or transport then the remaining D1.00 will be added to the D10.00b for the next shopping ..

Thank you Sidou Sanneh. Your true profit is D1.50 per unit. What I like about your approach is the fact that you are retaining part of the profit in the business. This will definately improve the growth of such business.

You presentation is genuinely, unambiguously, and unequivocally done… congratulations…! However, though, i’m not an expert in money matters, but through some reserches i’m able to know that wealth creation is no magic, it’s a formular… You see the reason why someone doesn’t create wealth, is either he/she doesn’t know the wealth creation formular or he/she can’t apply the wealth creation formular… You’ve made that part explicitly clear in your presentation, and is so interesting… Again i learnt that in creating wealth, one must be totally familiar with some financial terms as cashflow, expenses, asset, and liability… please, can you further elucidate these financial terms for the benefit of a layman like me… Thank you, and may Allah bless you always….

Thank you very much Alagie. We will prepare another article to explain some of these financial terms.

that’s true..you have spoken well..

Thank you Abdou Khadir Drammeh

you welcomed..the fact is that..all what u are saying is affecting our society…liability is too much.

you welcomed..the fact is that..all are saying is affecting our society…liability is too much.